China’s financial conditions are tightening in May

This report presents the May 2023 update on the Commodity Leading Index Monetary China (CLIMC, see Appendix for index description).

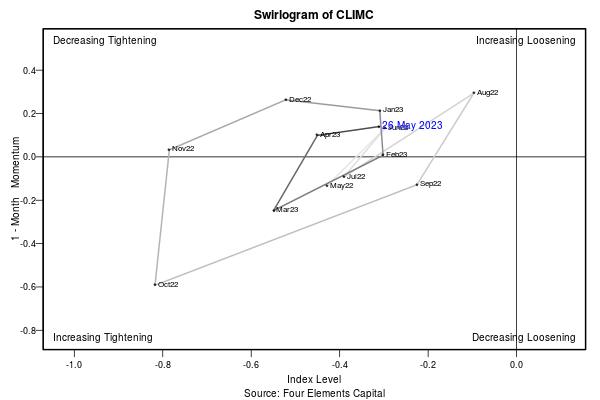

Decreasing Tightening Our CLIMC shows that financial conditions as of mid-April continues to tighten but at a slower pace. Consumer inflation fell to +0.1% yoy, though reopening pushed up services inflation, lower food and energy inflation, driven largely by base effects offset it. Producer inflation fell to -3.6% yoy, underlining the struggles for factories and the broader economy looking to rev up after the lifting of COVID-19 curbs. RMB is depreciating against the basket of currencies of main trade partner.

Correspondingly, as shown in the Swirlogram, the CLIMC places the financial environment in a decreasing tightening mode. The monthly index average of -0.31 is up by 0.14 over the month (one year range is -0.82 to -0.1) and is above the yearly average of -0.42.

Note: While the values of the previous months are calculated for the index average of the entire month, the value of the current month is estimated from the data available at the report release.

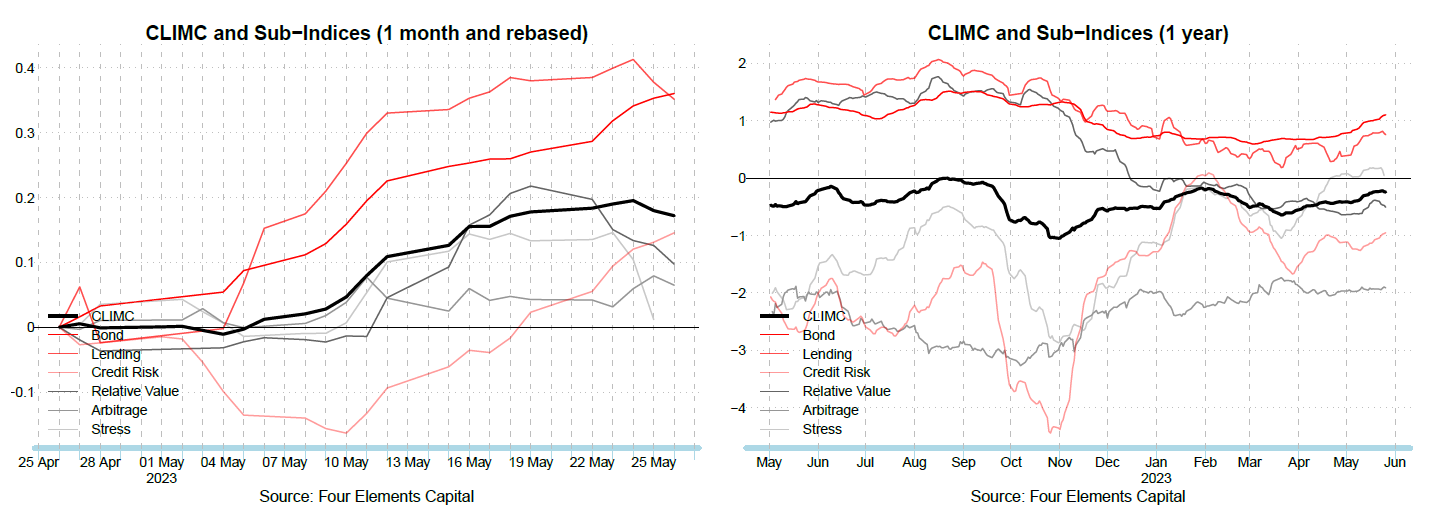

CLIMC and Sub-Indices Over the previous month, 3 sub-indices of the CLIMC increased, 3 sub-indices remained within the month-on-month momentum range of +/-0.1 standard deviations (s.d.) while none decreased.

On the positive side, the Bond, Lending and Credit Risk sub-indices increased due to decreasing (government) bond yields, decreasing interbank rates and decreasing default risks.

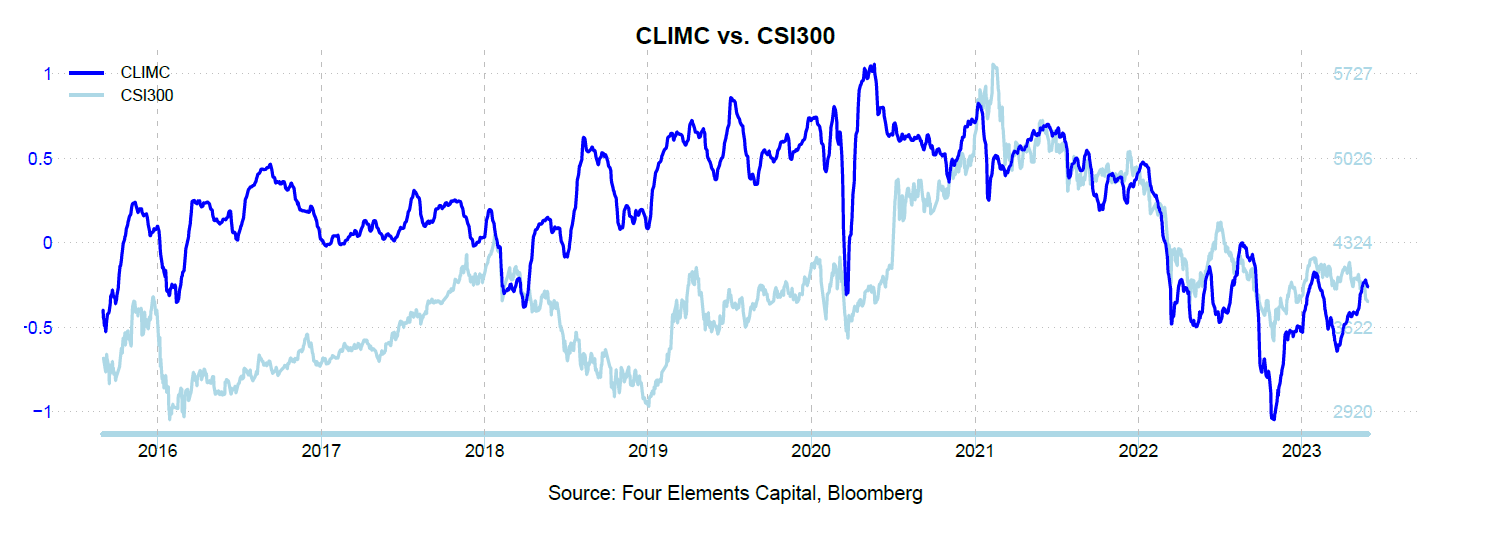

CLIMC vs. CSI300 The CLIMC correctly captured the major turning points in Chinese equity as measured by the CSI300 during the recent months. The improvement of the index in mid February 2016 has bolstered the markets in March 2016. The improved financial conditions which started in late June 2016 has led to the upward movement of the markets in August 2016. In addition, the weakening financial conditions since November has pointed to the end of the equity rebound in December 2016. The equity market then benefited from relatively loose financial conditions during the first three quarters of 2017. The tightening conditions that prevailed during the last quarter of 2017 and early 2018 weighted on the equity market. The acceleration of loosening conditions only began to support the equity market in 2019. Loosening financial conditions starting in April 2020 supported the equity market in the aftermath of the coronavirus, as shown in the graph below.

Disclaimer This material is solely for your information and use. It is not a solicitation or an offer to participate in any trading strategy. Investors should rely solely on fund documents in making investment decisions. This material does not constitute or form part of, and should not be construed as, any offer for sale or subscription of, or any invitation to offer to buy or subscribe for, any investments, nor should it or any part of it form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FOUR ELEMENTS expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) the use of this note, (ii) reliance on any information contained herein, (iii) any error, omission or inaccuracy in any such information. The price and value of investments mentioned and any income which might accrue may fluctuate and may fall or rise. Past performance is not necessarily a guide to future performance. This information and any related recommendations or strategies may not be suitable for you; it is recommended that you consult an independent investment advisor if you are in any doubt about any investments or investment services. Nothing in this material constitutes investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate to your individual circumstances, or otherwise constitutes a personal recommendation to you. If an investment is denominated in a currency other than your base currency, changes in the rate of exchange may have an adverse effect on value, price or income. The levels and basis of taxation may also change from time to time.

Appendix : Index Composition

CLIMC The Commodity Leading Index Monetary China (CLIMC) intends to be a representation of the overall financial liquidity in China. The CLIMC is a composite index of financial variables and includes six sub-indices. Each component is normalized and smoothed before aggregation and updated in the index as new information becomes available. The rolling standard score (Z-score) approach has been applied to normalize each component. As such, a reading above zero indicates loosening and below zero tightening of financial conditions relative to the mean. Upwards movements of the index indicate improving and downward movements deteriorating financial conditions. Each of the sub-indices has been smoothed by the exponential moving average procedure to remove noise from the components. The CLIMC is composed of six sub-indices with equal weighting:

-

Stress sub-index

-

Credit Risk sub-index

-

Lending sub-index

-

Bond sub-index

-

Relative Value sub-index

-

Arbitrage sub-index

Stress sub-index The CLIMC Stress subindex (CLIMCS) intends to capture the level of risk aversion measured by general market volatility. An increase of the CLIMCS means less stress and thus loosening financial conditions.

Credit Risk sub-index The CLIMC Credit Risk sub-index (CLIMCCR) measures regional credit healthiness. The higher the CLIMCCR, the lower the credit default risk which represents a loosening factor.

Lending sub-index The CLIMC Lending sub-index (CLIMCL) is a composite index of relevant short term regional rates. A higher level of the CLIMCL indicates lower lending cost which reflects a loosening factor.

Bond sub-index The CLIMC Bond subindex (CLIMCB) represents the long term government bond prices and debt securities. A higher level of the CLIMCB is associated with lower average market yields, and thus cheaper long-term financing, implying a loosening effect.

Relative Value sub-index The CLIMC Relative Value sub-index (CLIMCRV) intends to assess the market expectations on the monetary situation versus current conditions, in particular whether current market conditions are tightening or loosening relative to market expectations. An increase of the CLIMCRV indicates a likely change toward a loosening situation.

Arbitrage sub-index The CLIMC Arbitrage sub-index (CLIMCA) approximates the margin of engaging in RMB arbitrage transactions, thus providing a measure of hot money inflows (outflows) that contribute to loosening (tightening) of financial conditions in China. A surge in the CLIMCA corresponds to an increase in arbitrage margins favoring hot money inflows into China and vice versa.